Rent Vs. Buy: Five Reasons Buying is Still the Best Option

For those seeking a new house to call home, contemplating renting versus buying can seem overwhelming. The fact is, buying a home is a lot more attainable than many realize. Even as interest rates rise, homeownership continues to offer significant financial benefits, and with many loan options to consider, buying might be easier than you think.

Here are five reasons you should purchase, rather than rent, your next home:

1. Homeownership is an investment and a key component to building long-term wealth.

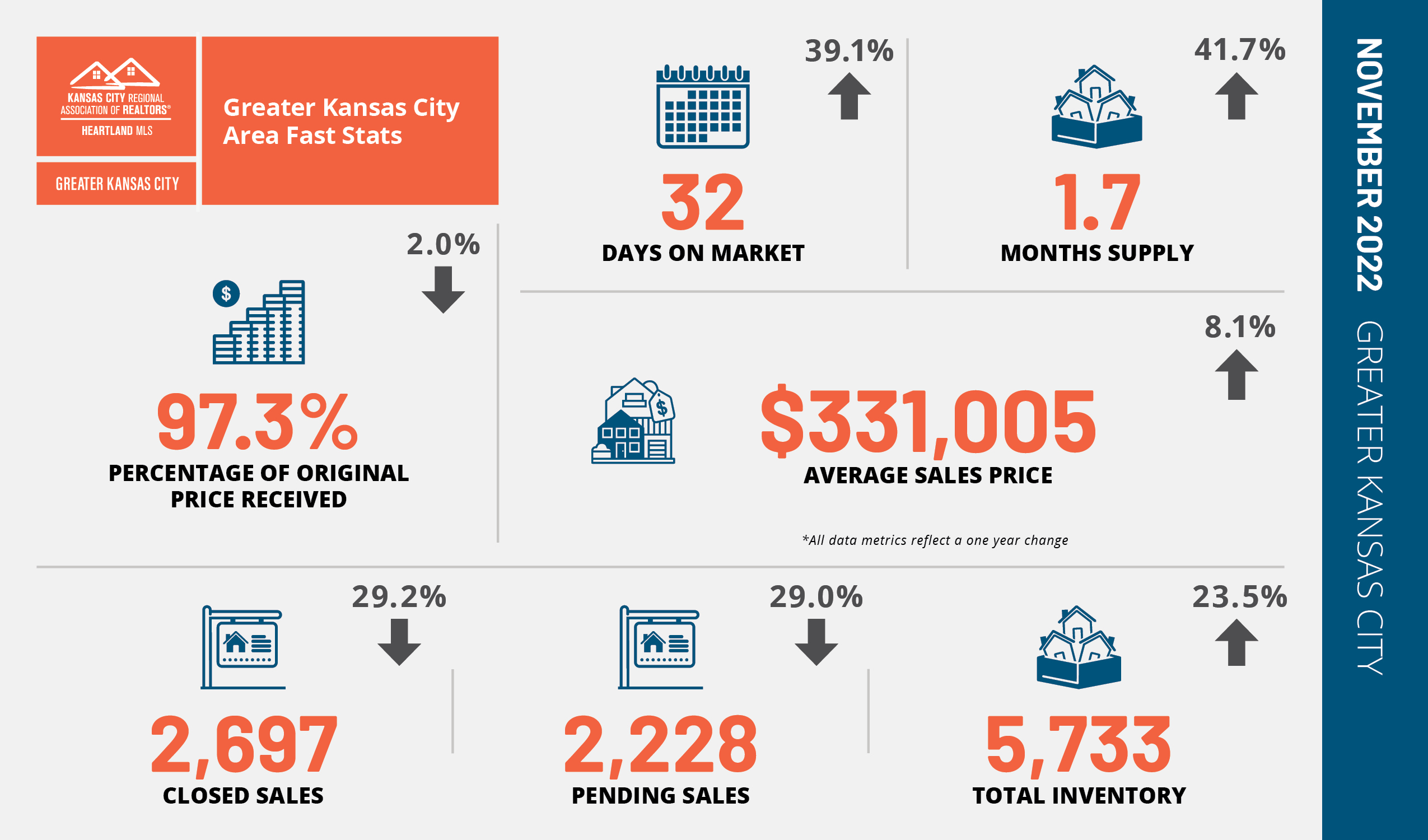

Homeownership is the ideal “forced savings” plan, with each monthly mortgage payment acting as an investment in your own wealth, not your landlord’s. As you continue making payments, you build equity over time, which, coupled with the property’s appreciation, yields some of the best returns available from any investment. According to the National Association of Realtors, someone who purchased a home 10 years ago at the median price of $169,000 accumulated $225,000 in home equity on average. Eighty-six percent of that equity came from price appreciation, thanks to a 7.9% annual increase in home prices nationally. Closer to home, Heartland MLS reports that average sales prices are up 8.1% year over year in the Greater Kansas City area, making homeownership a robust and reliable investment in your future.

{kind=link}

2. Owning a home means the freedom to make it your own.

Renters know all too well the challenges of customizing their homes to suit their needs. Once you buy a house, however, you’re free to customize, remodel and decorate your new home to your heart’s content. Change your paint color with your mood. Plant a garden for every season. Enjoy the freedom to have the pets you want, plus a yard for them to play in. As a homeowner, you can feather your nest however you see fit.

3. Homeowners enjoy a stable, predictable monthly payment.

With no rent control laws, Kansas City renters are subject to whatever increases their landlords wish to levy at the end of their leases. For most renters, that means an increase in their monthly housing costs each and every year. In fact, the average rent for a one-bedroom apartment in Kansas City, Missouri, grew 13% in the last year. However, with a fixed-rate mortgage, homebuyers know exactly how much their loan payment will be for the life of the loan. Furthermore, they might even be able to reduce their payment by refinancing to a lower rate in the future. Use a mortgage calculator to estimate loan payments in your price range.

4. Monthly costs may be lower than renting, and down payments aren’t as daunting as you think.

A common misconception among first-time homebuyers is that you need a 20% down payment to purchase a home. The fact is, there are many loans available that can bring that figure down to 5%, 3% or even 0%, including FHA, VA, Fannie Mae, and Freddie Mac programs. Be sure to reach out with any questions about down payment options.

With the down payment cleared up, you can now focus on the monthly mortgage payment cost. While rents can rise unabated, you can lock in your mortgage cost for years to come or even reduce it. Even though mortgage rates have risen sharply in recent months, they are still well below what a homeowner would’ve expected to pay 20 or more years ago. Plus, with options like an Interest Rate Buydown, monthly rates are often lower than expected.

An Interest Rate Buydown reduces the monthly mortgage payment through a seller credit. For example, a temporary buydown uses a seller-paid credit held in an escrow account that the homebuyer can use to buy down the interest rate by 2% in the first year and by 1% in the second year. The rate can be refinanced at any point throughout the life of the loan. Any unused portion of the credit is applied to the loan balance, so nothing is left on the table. We have many trusted local mortgage lenders to recommend and discuss your options. Contact us to learn more.

5. Owning a home can mean significant tax benefits.

While each person’s tax picture is unique, there are numerous potential tax savings for homeowners that renters do not have. Many homebuyers can leverage deductions for mortgage interest, private mortgage insurance, property taxes, home improvements, and home office use to lower their overall income tax bill. Speak to your tax professional to learn more about your possible benefits.

We can help you navigate the home-buying process

If you’re contemplating buying or renting your new home, we’d be happy to help you navigate your options. If homeownership is right for you, we can connect you with a local mortgage lender to get you pre-approved and lay the foundation for your home search! Contact us today to start your home-buying journey.